Katie Evans is Head of Research and Policy at the Money and Mental Health Policy Institute. She previously led a programme of work around financial services at the Social Market Foundation and has also been an economic consultant. She spoke at MALG’s National Members Meeting on 5 July and shares her insights from the group discussion she led in this blog:

I was pleased to be asked to deliver an interactive session at the Money Advice Liaison Group’s (MALG) National Members Meeting on 5 July 2017. For me, it was a unique opportunity to get in front of a diverse group of advisers, creditors, collections professionals, and other stakeholders to get their insight on some of the key policy areas we’re currently looking at.

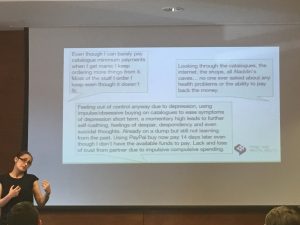

After presenting Money and Mental Health Policy Institute’s initial findings on the difficulties being experienced by people with mental health problems around point of sale credit products, I split attendees into groups to discuss both what could be driving these problems and some potential solutions.

After presenting Money and Mental Health Policy Institute’s initial findings on the difficulties being experienced by people with mental health problems around point of sale credit products, I split attendees into groups to discuss both what could be driving these problems and some potential solutions.

It was acknowledged before discussion began that the big fix in this area would be to create a system whereby people who know that their mental health makes them more vulnerable to taking out unaffordable credit could self-exclude for a set period of time. This macro solution will take time, however, and so the group discussed the possibility of shorter-term interventions.

The three questions discussed were:

- What is specific about the way credit products are sold at the point of sale? Are there any other potential reasons why people get into problems with these products?

- It’s no longer permissible to offer discounts in the first seven days a store card is opened. Should this practice be ended for other point of sale products too?

- How can we clarify credit pricing and contract terms to ensure understanding when credit is sold alongside another product?

A short summary of the discussion on each question is included below.

1) What is specific about the way credit products are sold at the point of sale? Are there any other potential reasons why people get into problems with these products?

The group discussed a wide range of characteristics of point of sale products which can cause problems.

The emotional consequences of wrapping credit up with another product were discussed at some length. Several participants noted that once credit is tied to an object, the focus of the purchase is that thing, not the credit product. The focus of the decision is on the characteristics of the object, not on the nature of the credit product.

In the case of hire purchase, particularly on white goods, it was noted that replacements are a priority, and that for those consumers using this type of credit because it’s all they can access, time will be of the essence. There may not be space for further reflection on the terms of credit; securing a replacement freezer or washing machine today might be more compelling. This is also linked to the type of consumers using these products, who tend to be relatively low income and otherwise financially excluded.

It was also noted that access to credit makes it harder for those without financial means to limit themselves to window shopping, which might be particularly problematic for people experiencing mental health conditions associated with increased impulsivity.

Tying credit to the purchase of an item can also make cancelling the credit contract more difficult – both because the item is already in your possession, and people with mental health problems are likely to find returns processes more difficult to navigate, and because unlike a loan which you may spend a few days after it comes in, the money is gone immediately so any cooling off period for the credit needs to factor in the returns process for the item.

The group also briefly discussed the conditions or incentives attached to purchases, particularly in car finance, and the complexity of pricing of point of sale credit (pay XX for 8 weeks, then XX for a year etc).

MALG MM July 2017 – MMHPI video from Bob Winnington on Vimeo.

2) It’s no longer permissible to offer discounts in the first 7 days a store card is opened. Should this practice be ended for other point of sale products too?

This question received a resounding yes from the group. Dissenters were invited to respond by email if they had counterarguments, but to date no further responses have been received.

3) How can we clarify credit pricing and contract terms to ensure understanding when credit is sold alongside another product?

Various ways to illustrate the costs of credit more effectively were put forward by the group. Two major themes were that the total cost of credit if all payments are made on time should be clearly showed as £ figure, alongside the total cost if it isn’t paid off on time or payments are missed. We did, however, note the potential weaknesses of this kind of framing, as most people will assume that the worst-case scenario will not apply to them. Grounding that in a real figure, however, could be very beneficial. One group also suggested that sliders could help online customers explore the ways that the costs of credit could vary.

We also briefly discussed how “buy now, pay later” models could be clarified to ensure consumers understand the potential costs involved. Showing a spread of possible costs, or the proportion of people who end up paying for this credit, could be helpful.

One group noted that displaying this price information visually – potentially in comparison to the cost of the good being purchased, could be very helpful in providing customers with a sense of perspective.

There was a general awareness throughout the discussion that more information that has to be read to a customer at the point of sale isn’t always an effective way of getting a message across, and equally that pop-ups in online application processes can easily be overlooked even when active participation is required to move forward. Rigorous testing would be needed to identify the most effective information remedies in these markets.

The intricacies of affordability checks for notionally ‘free’ credit products were also discussed – do these loans check not just that a person can afford the repayments of the principle, but that they would be able to afford interest payments too if they don’t repay within the initial term or miss a payment.

We’ll now be using the insights gained from this MALG session in the development of our policy work in this area. Watch this space.